How to Backtest ICT Strategies: Complete Guide to TradingView Replay

Backtesting is how you prove your edge before risking real money. Learn the exact system to backtest ICT strategies on TradingView with templates, checklists, and data tracking.

Every trader believes their strategy works. Most are wrong. Backtesting is how you find out BEFORE risking real money. After 100 backtested trades, you will know your actual win rate, average R:R, maximum drawdown, best setup type, and whether you actually have an edge. Without backtesting, you are gambling with a theory.

What You Need to Backtest

You need TradingView Premium (or free with limitations) for replay mode, a backtesting journal in Google Sheets or Excel with columns for date, pair, setup, entry, stop, target, result, and emotions, and your exact rules written down including entry criteria, exit criteria, risk per trade, and killzone rules.

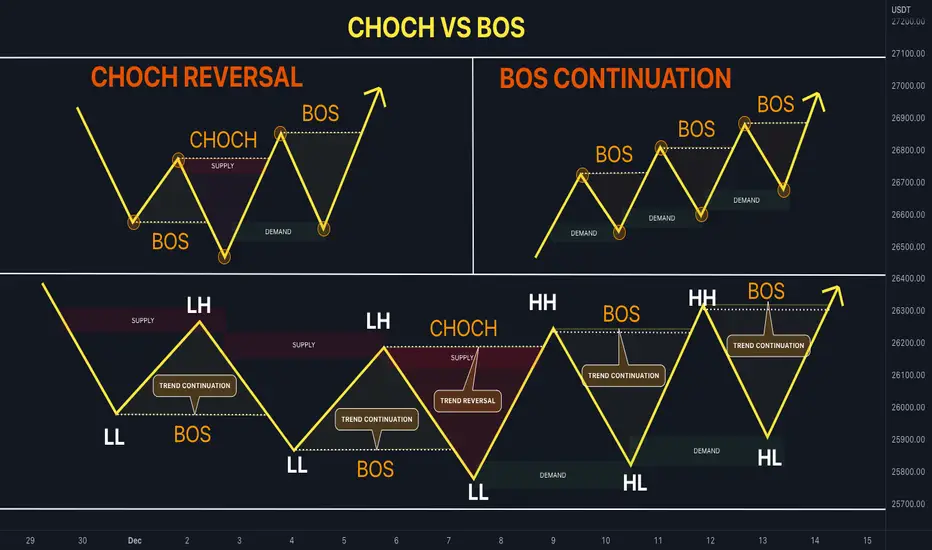

The ICT Backtesting System

Step 1: Choose ONE strategy to backtest. Do not mix strategies. Options include Silver Bullet, Order Block plus FVG confluence, Breaker Block reversals, or SMT Divergence setups. Step 2: Set up TradingView Replay. Open TradingView, select your pair, click replay, set date 6 months ago, and hide future candles. Step 3: Mark higher timeframe structure including daily dealing range, daily bias, BSL and SSL levels, and current trend before moving bar by bar.

Backtesting Rules (Critical)

No cheating -- do not look ahead at future candles or change rules mid-backtest. Skip nothing -- record every triggered setup including losing ones. Be honest about emotions even in backtesting. Track everything including setup type, entry, stop, target, result, R:R, whether rules were followed, emotions, mistakes, and market condition.

Backtesting Statistics to Calculate

Win rate: wins divided by total trades times 100. Expectancy: (win rate times average win R) minus (loss rate times average loss R). A positive expectancy equals a profitable strategy. Maximum drawdown: largest peak-to-trough decline. Profit factor: gross profits divided by gross losses. Above 1.5 is good. Above 2.0 is excellent.

ICT-Specific Backtesting Focus

Test these specific questions: What percentage of wins came during killzones vs outside? Which PD array had the highest win rate -- OB, FVG, or Breaker? What was your win rate buying in discount vs premium? What was your win rate trading WITH daily bias vs against it? Results will show which filters to require and which to exclude.

Common Backtesting Mistakes

Curve fitting: adjusting rules to fit historical data perfectly creates a strategy that fails in the future. Small sample size: 20 trades tells you nothing. Only cherry-picking winners: test every valid setup. Only testing bull markets: test across all conditions. Not simulating execution: subtract 1-2 pips from every win to simulate real spread costs.

Backtesting Schedule: Weeks 1-2 define your strategy and rules. Weeks 3-6 backtest 100 trades at 10-15 per week. Week 7 analyze all statistics and find patterns. Week 8 refine one rule at a time and re-test. Then forward test on demo at 0.5% risk for 50 trades. Spend 100 hours backtesting before risking $1000 live. Your future self will thank you.